This white paper offers an exclusive preview of JointValues’ research into ESG disclosures by India’s top 1,000 listed companies under SEBI’s mandated Business Responsibility and Sustainability Reporting (BRSR) framework for FY 2023–24.

The data was manually collected and systematically analysed by the team of research associates during the third and fourth quarters of FY 2024–25. Various visuals from the analysis of data highlights sector-wise performance, disclosure quality, emerging good practices, and areas for improvement.

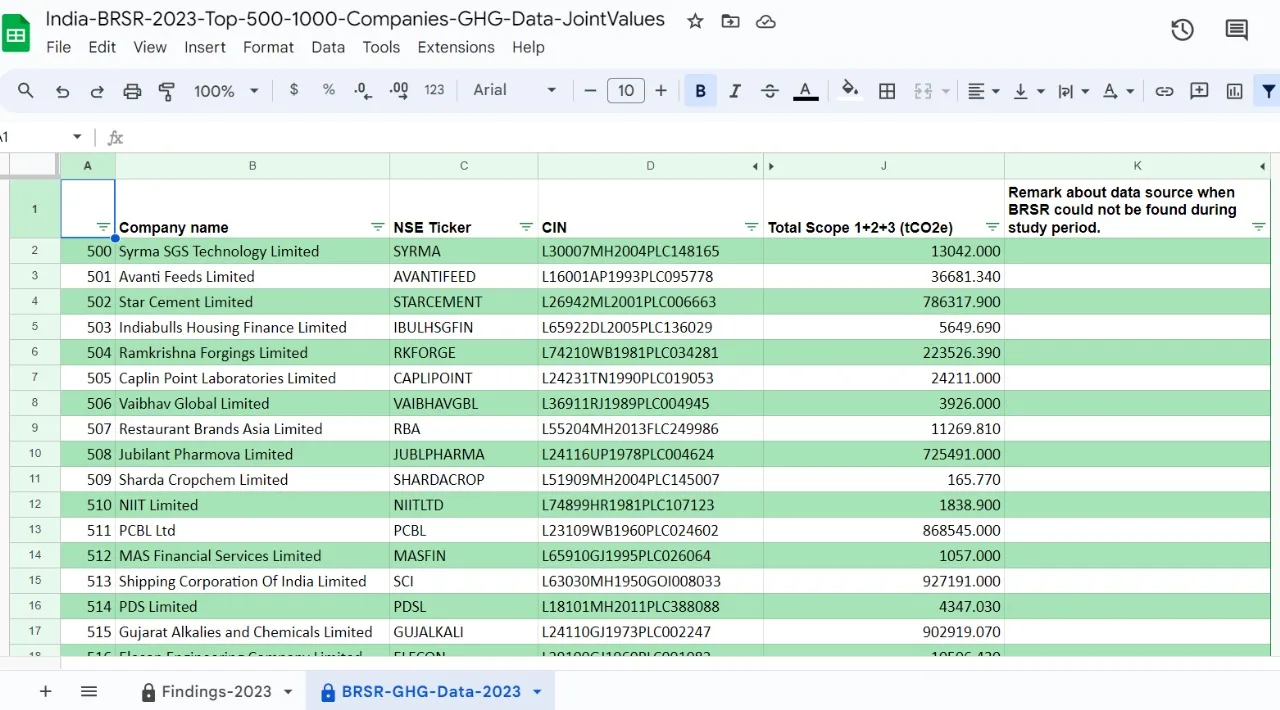

This preview focuses on the sectoral distribution of the top 1000 listed companies mandated to submit disclosures under SEBI’s Business Responsibility and Sustainability Reporting (BRSR) framework for the financial year 2023–24.

The data, derived from 978 companies whose BRSR disclosures were available at the time of study, categorizes entities based on their primary sector of economic activity. Classification is based on the National Industrial Classification (NIC) system, using BRSR Indicator 7.3 (primary product/service accounting for at least 90% of turnover).

Sector-wise Distribution: Key Highlights

The following sectors represent the distribution of companies reporting under BRSR:

- Manufacturing: 54.8%

- Financial and Insurance Activities: 12.5%

- Information and Communication: 8%

- Wholesale and Retail Trade; Repair of Motor Vehicles: 4.7%

- Construction: 4.4%

- Electricity, Gas, Steam, and Air Conditioning Supply: 2.9%

- Professional, Scientific, and Technical Activities: 2.8%

Remaining sectors (including education, public administration, healthcare, water supply, and others): each account for less than 2.5% individually.

Strategic Insights

- Manufacturing Dominance

Over half of the companies fall within the manufacturing sector, reaffirming its central role in India’s corporate ESG landscape. This presents a significant opportunity to drive sustainability transformation through focused policies, resource efficiency, and emissions management. - Financial Services as ESG Catalysts

The second-largest group comprises financial and insurance institutions (12.5%), positioning the sector as both a disclosure participant and a key enabler of ESG integration across capital markets. - Broad Sectoral Representation

Although manufacturing and finance dominate, the data reveals participation across diverse sectors, including IT, retail, construction, utilities, and services. This reflects a growing maturity in ESG adoption beyond traditional industrial players.

Implications for Policymakers and Business Leaders

- Targeted Policy Support: Given the concentration of disclosures in manufacturing and finance, sector-specific ESG guidelines may be needed to drive deeper integration and comparability.

- Sectoral Benchmarking: Industry-wise ESG benchmarking will be critical in evaluating relative performance, identifying gaps, and aligning disclosures with global best practices.

- ESG Integration Across the Economy: While some sectors remain underrepresented, their inclusion highlights the expanding reach of sustainability reporting mandates, which will require tailored ESG frameworks to address sector-specific nuances.

Looking Ahead

As India’s ESG reporting landscape matures under the BRSR mandate, a more nuanced understanding of sector-wise trends will be essential. The forthcoming full report from JointValues is expected to provide deeper insights into disclosure quality, materiality assessment, and sectoral readiness—supporting investors, regulators, and corporate boards in strategic decision-making.

Authors

Dr Swathi Karamcheti

Mr JS Kamyotra