This white paper offers an exclusive preview of JointValues’ research into ESG disclosures by India’s top 1,000 listed companies under SEBI’s mandated Business Responsibility and Sustainability Reporting (BRSR) framework for FY 2023–24.

The data was manually collected and systematically analysed by the team of research associates during the third and fourth quarters of FY 2024–25. Various visuals from the analysis of data highlights sector-wise performance, disclosure quality, emerging good practices, and areas for improvement.

This preview focuses on the reporting boundary adopted under the mandatory Business Responsibility and Sustainability Reporting (BRSR) framework introduced by SEBI.

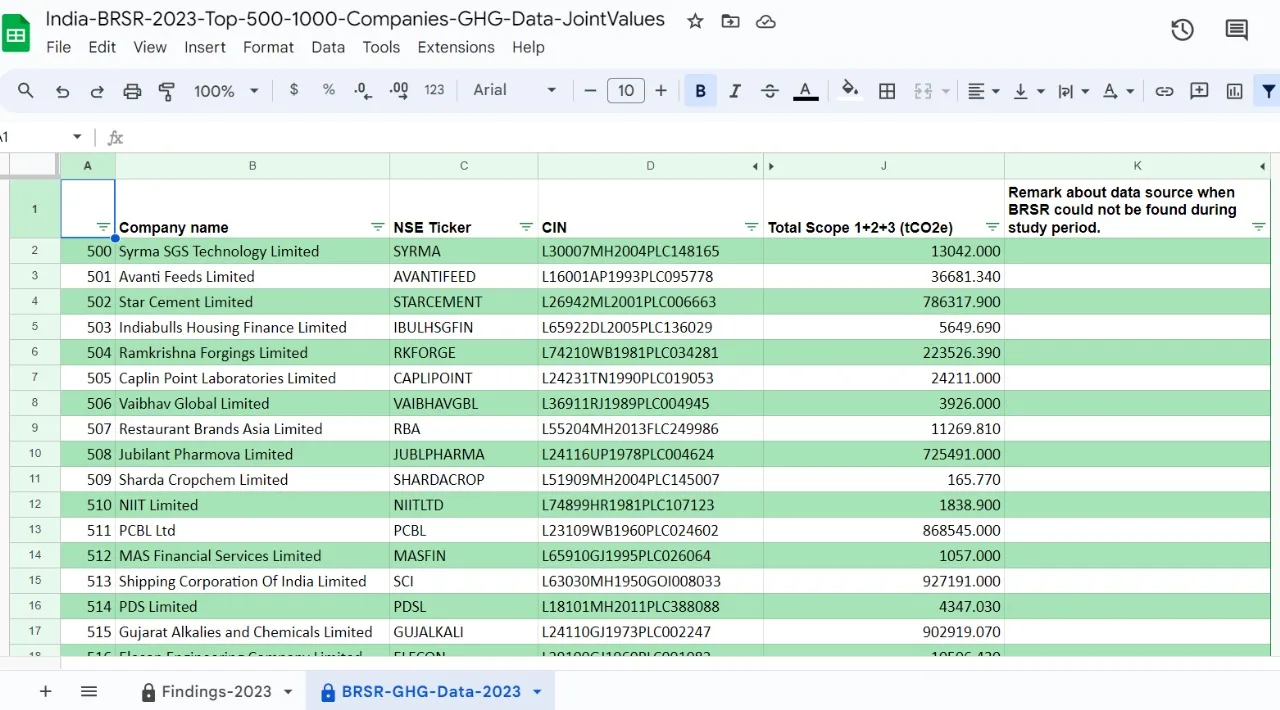

Based on data from 978 companies whose BRSR disclosures were available at the time of analysis, the reporting boundary distribution is as follows:

- 84.6% of companies disclosed ESG data on a Standalone basis.

- 15.4% of companies reported on a Consolidated basis.

Key Insights

- Predominance of Standalone Reporting

A significant majority—over four-fifths—of companies continue to disclose ESG data solely for their standalone legal entity. This approach excludes subsidiaries, joint ventures, and affiliated entities. While it meets minimum compliance requirements, it may not fully capture the broader environmental and social footprint of diversified or group-based businesses.

- Limited Adoption of Consolidated Reporting

Only 15.4% of companies have adopted a consolidated reporting boundary, which encompasses the full corporate group. This more comprehensive approach aligns more closely with international ESG expectations and provides a clearer view of overall sustainability performance. The limited adoption indicates that holistic ESG transparency remains an emerging practice in India.

- Implications for Stakeholders

The current reporting trend reveals a notable gap in comprehensive ESG disclosure. This may impact:

- Investor confidence, due to incomplete visibility into group-level risks and impacts;

- Regulatory oversight, as policymakers increasingly emphasize integrated sustainability reporting; and

- Sustainability benchmarking, where fragmented data may hinder comparability and performance tracking.

Looking Ahead

As global ESG expectations continue to evolve, the transition from standalone to consolidated disclosures will likely emerge as a strategic imperative for boards, CFOs, and sustainability leaders aiming to strengthen corporate transparency, accountability, and stakeholder trust.

Authors

Dr Swathi Karamcheti

Mr JS Kamyotra